What Economic Price for Democracy in Africa?

It may not be high at all once a basic threshold of income is reached, and provided elections are properly conducted

It may not be high at all once a basic threshold of income is reached, and provided elections are properly conducted

On the face of it, democracy is on the rise in Africa. According to Freedom House, notwithstanding a not insignificant coterie of failed states, out of a total 53 African countries, there are now 19 full electoral democracies on the continent. (Of course, the question of democratic versus non-democratic values outside of elections is vexed.)

Since the democratic elections in Namibia in 1989, well over 30 ruling parties in Africa have changed on the strength of national elections. Contrast this with the lone peaceful transfer of power on the continent – in the event, in Mauritius – between 1960 and 1989, a period during which only five countries held regular elections.

In per-capita terms – with population growth still rising – and at purchasing power parity, gross national income has risen in Africa by over a third since 2000. Forecasts remain optimistic, with the IMF projecting that 11 of the world’s top 20 fastest growing economies through to 2017 will be African. It might be tempting, therefore, to conclude that there is a virtuous relationship between democracy and economic growth and development. Yet the interplay between the two is far from clear cut. During the past five years, while African growth has in many cases been impressive – even in the context of the global financial crisis – democratic progress has tapered off. Freedom House has reported a drop of five full electoral democracies (in the event, since 2005), and the Mo Ibrahim index has reported a drop of five percent in political participation since 2007.

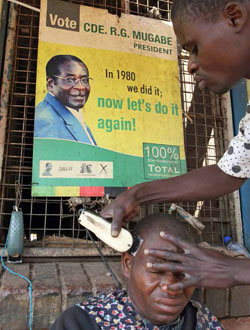

Major challenges remain. Full electoral democracies are still in the minority in Africa. Robust economic growth is unevenly distributed, with some democracies like Mali facing both democratic and economic crises, while less democratic countries like Angola have experienced economic booms. Moreover, where democracy and economic growth have interacted most directly – around election time – the impact of democracy on economic growth and development has not always been positive. For instance, Ghana’s growth dropped from 15 percent in 2011 to 7.9 percent in 2012, the election year. In Zimbabwe, the drop was 4.3 percent ahead of the 2013 presidential election.

The impact of electoral cycles can also extend to economic policy decisions. After the 2008 Ghanaian election, for instance, the new ruling party reassessed many existing contracts – especially in the construction sector – withholding payment for up to two years in some cases. Non-performing loans in Ghana’s banking sector soon more than doubled to 18 percent. In Zambia, the new government reversed the privatization of Zamtel, and made a surprise policy announcement to introduce additional capital requirements for the banking sector. This prompted Fitch to revise its rating outlook to negative, and raised the risk perceptions of foreign investors. Still, both countries later managed to place bonds in the international markets. In both instances, the bonds were several times oversubscribed.

So what is the economic price of democracy in Africa? The question demands careful treading. For one, we might distinguish between the direct economic cost of democracy – such as election costs – and the economic price of democracy. The ‘price of something’ is commonly taken to be an unwelcome experience, event or action involved as a condition of achieving a desired end. That there is a direct economic cost of democracy is manifest. In Africa, this cost can be substantial – at times higher than in the West. For example, the Australian election of 2010 is estimated to have cost about US $160 million, whereas the historic 2006 elections in the DRC are estimated to have cost well over US $400 million – over 50 percent more expensive per registered voter in absolute terms, and substantially more in purchasing power parity terms.

What about the economic price? Oxford’s Paul Collier has done extensive theoretical and empirical work that partially addresses this question. He paints a complex picture of the interaction between democracy, security and (economic) policy improvements that may ultimately foster growth. He and his colleagues studied data for over 786 elections in 155 countries. In one interesting conclusion, they estimate that elections make societies safer only when these societies exceed an income-per-capita threshold of US $2,700. Security and stability tend to be helpful to businesses, so this finding lends credence to the idea that democracy can help boost economic growth and development. However, the effect apparently only kicks in after economic growth and development have brought a country well above the middle-income country threshold. As such, the projected robust economic growth of many African countries could well help to reduce the security price of democracy in Africa.

At the same time, the research finds that democracy comes with certain economic benefits – in particular, that frequent elections produce structurally better economic policy. Net of electoral cycle effects, more elections are on average positive for policy – a relationship that Collier and his team attribute to better accountability. (Surely, however, it cannot be that endless elections in short intervals conduce to better economy policy.) However, the research also finds that this effect is only robust for properly conducted, non-fraudulent elections. After all, fraudulent elections are less likely to lead to accountability vis-à-vis the populace. On this score, a number of African countries have less than fortunate starting positions, with income below the appropriate threshold and elections that are, for the time being, poorly conducted. The Collier theory predicts for these countries not only a monetary cost of elections, but also a non-negligible security cost to be paid for democracy – without the concomitant benefits from improved economic policy.

An on-the-ground perspective gained from investing in the continent paints a more positive picture. According to Ernst & Young’s 2013 Africa attractiveness survey, 86 percent of investors who already do business on the continent rank Africa as the second most attractive regional investment destination in the world – after Asia. Interestingly, the survey also suggests that African democracies with per-capita income levels well below the US $2,700 threshold are disproportionately favoured by international investors. These countries include Ghana, Nigeria, Zambia, Tanzania and Kenya. Of the top destinations mentioned, only South Africa qualifies as a country with a functioning democracy and per-capita income exceeding the said threshold. Still, the majority of the remaining countries do hold regular elections. And with the exception of the December 2007 elections in Kenya, these elections have been quite peaceful.

Anecdotal evidence from my own experience in financing projects in Africa suggests that positive investment decisions do appear to benefit from the democratic credentials of African countries. Democratic accountability of governments to their people is perceived to be accompanied by better rule of law, more transparency, and less corruption – all of which aid foreign direct investment. With the advent of the OECD guidelines for responsible business, increased pressure on investors from NGOs, as well as the tightening of regulatory standards in anti-money laundering and corruption, it seems likely that investor decisions will be increasingly influenced by the interplay between democracy and economic development. This tendency may well serve to reduce the price of democracy in those countries where it is potentially present.

From a policy perspective, the potential for a virtuous cycle of more democracy, investment and economic growth could be strengthened in several ways. International investment, which tends to be sensitive to violence and, increasingly, to political corruption, can help to raise the price of bad economic policy and electoral turbulence. Especially in higher-risk countries and nascent democracies, development banks, with their stable capital base and long-term planning perspectives, can, and already do, play a constructive role by investing throughout and across the electoral cycle. This effect can be strengthened by levering democratic institutions in the context of the investment process. In Ghana, for instance, development banks and commercial banks typically require parliamentary approval for large investment projects – as in, say, the power sector. To manage the electoral cycle of economic growth, increased central bank independence can help to address the monetary side of the problem. Addressing the fiscal and economic policy side of the cycle is more challenging. Capacity development programmes aimed at raising politicians’ awareness of the costs involved could be a start. According to an IMF study, another successful intervention could be to institute fiscal rules – conceptually similar to the Excess Crude Account in Nigeria – that can reduce the political flexibility required for opportunistic spending. The effectiveness of these rules could be strengthened by real-time feedback from external rating agencies: consider Fitch’s change in outlook for Zambia in response to its unpredictable economic policy.

Bref, there is clearly a cost to democracy: a direct cost, and also an indirect cost caused by periodic electoral instability – instability that can temporarily affect foreign investment decisions. Nevertheless, net of economic benefits, the case that there is an economic price of democracy across Africa appears weak. If there is a threshold of per-capita income below which this could be the case, anecdotal experience suggests that this threshold may be falling, as democratic countries exploit benefits in attracting international investors. Indeed, a new trend appears to be emerging in Africa – one where the combination of economic growth, responsible investors, and more experience in the conduct of democratic elections creates a virtuous interplay between democracy and economic development.

![]()

Jorim Schraven is Manager, Credit Analysis, and past Manager of the Financial Institutions – Africa Department at FMO, the Dutch development bank, in The Hague.